Florida’s unique geography—surrounded by water on three sides, with low-lying terrain, numerous rivers, lakes, and a porous limestone foundation—makes it particularly vulnerable to flooding from heavy rains, hurricanes, storm surges, and even king tides. Most of Florida is considered to be in a flood zone in one form or another, meaning that nearly every property in the state faces some level of flood risk, even if it’s classified as low or moderate. People aptly note that “all of Florida is in a flood zone,” emphasizing that flooding can occur anywhere due to the state’s flat landscape and weather patterns, regardless of official designations. Flood risk in Florida is mapped by the Federal Emergency Management Agency (FEMA) through Flood Insurance Rate Maps (FIRMs). These maps divide areas into zones based on the probability and severity of flooding, primarily tied to the Special Flood Hazard Area (SFHA), where there’s a 1% annual chance (or “100-year flood”) of flooding. Key FEMA Flood Zones in Florida. Insurance rates are standardized, you don’t need to shop them. Here are the primary ZONES:

- High-Risk Zones (SFHA – Mandatory Flood Insurance for Most Mortgages)

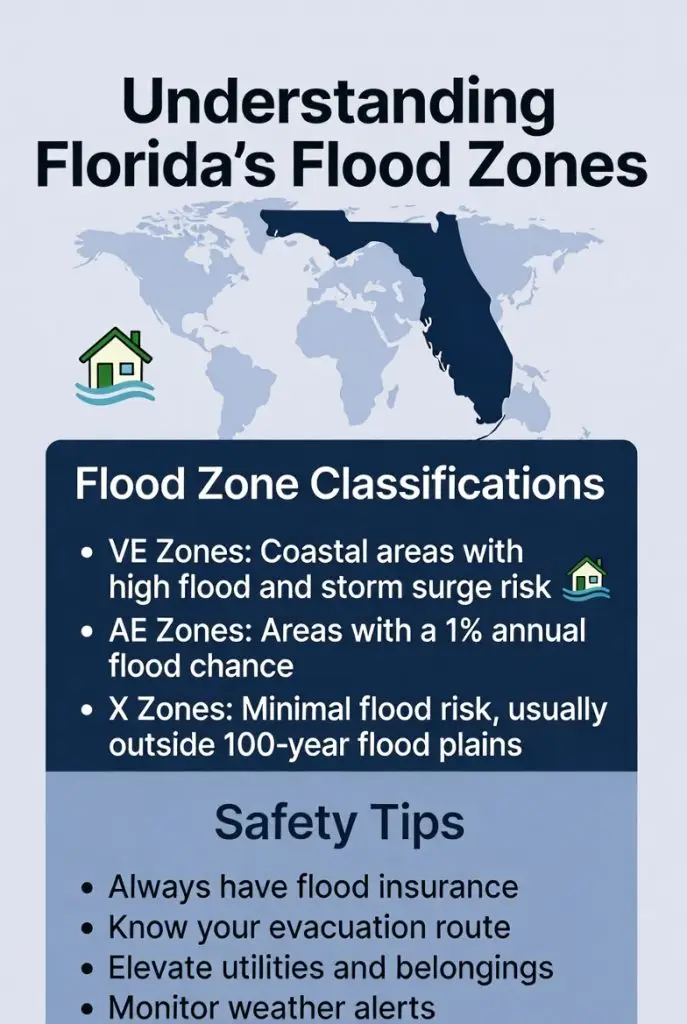

These areas have the highest flood probability and often require flood insurance if you have a federally backed mortgage.- Zone AE: Common across Florida, including inland and some coastal areas. These zones have a 1% annual chance of flooding, with a determined Base Flood Elevation (BFE)—the height floodwaters are expected to reach in a base flood event. Strict building standards apply, such as elevating structures above the BFE.

- Zone VE (Coastal High-Hazard Areas): Found primarily in coastal areas along the Gulf of Mexico, Atlantic Ocean, and bays. These zones face the same 1% annual flood risk but with added dangers from storm-induced velocity wave action (waves over 3 feet). They require the strictest construction rules, like building on pilings to allow waves to pass underneath, to withstand surge and erosion.

- Moderate- to Low-Risk Zones

- Zone X (shaded): Moderate risk, often between the 1% and 0.2% (500-year) floodplains. Flood insurance is not mandatory but recommended, as over 20% of National Flood Insurance Program (NFIP) claims come from these areas.

- Zone X (unshaded): Minimal risk, outside high- and moderate-hazard areas. Still, flooding can happen from localized events.

Even in Zone X, Florida’s weather can lead to surprises—rainfall alone can cause flooding in non-coastal areas.

Elevation Certificates: Essential When insuring a home in a flood zone. When purchasing a home in Florida—especially in a high-risk zone—an Elevation Certificate (EC) is a critical document. This official form, completed by a licensed surveyor or engineer, details your property’s location, flood zone, and crucially, the elevation of the lowest floor relative to the BFE. Why it matters:

- It determines compliance with local floodplain regulations.

- It helps calculate accurate NFIP flood insurance premiums—even small differences in elevation (just 1-2 feet) can significantly lower or raise costs.

- For new builds or homes in high-risk zones, lenders or insurers often require one.

- When buying, request the seller’s existing EC (if available) or obtain a new one to avoid surprises on insurance rates or required elevations.

In high-risk areas, an EC is often needed to secure insurance or permits, and it can reveal opportunities for premium discounts if the home is elevated properly.Navigating Florida’s flood zones can feel overwhelming, but understanding them empowers smarter decisions. If you’re considering buying a home—new construction or existing—and want expert guidance on flood zones, insurance implications, elevation requirements, and finding properties that fit your needs, New Build Buyer Realty can help. Their team specializes in guiding buyers through Florida’s real estate landscape, including the complexities of flood risks in this uniquely vulnerable state. Reach out to them for personalized assistance in securing your dream home safely and affordably.